Sugar Talk

Sugar Talk

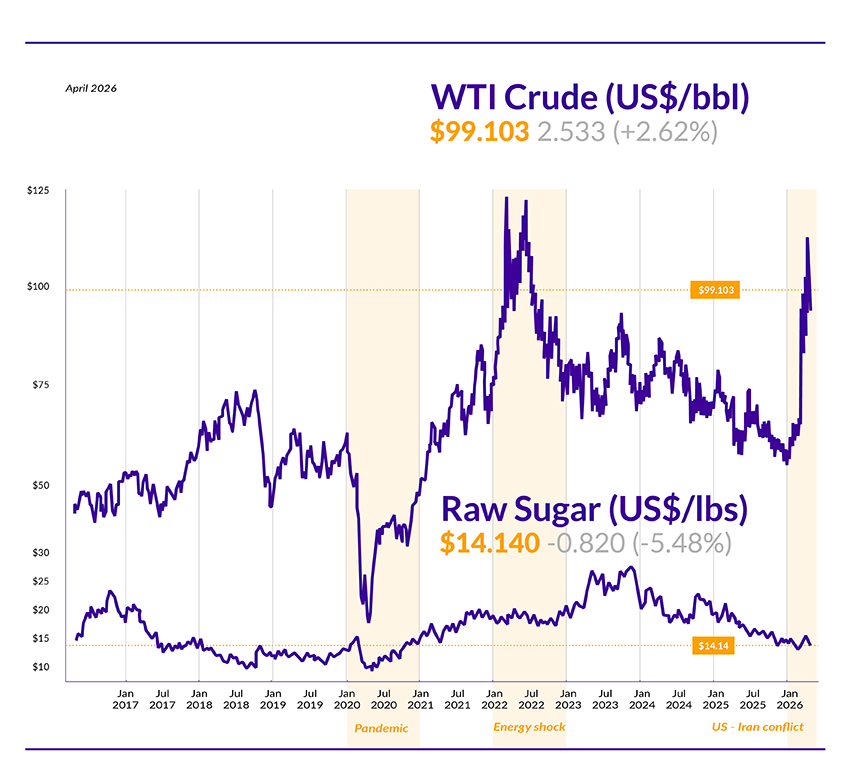

Why oil prices are driving sugar markets more than you think

Sugar buyers are used to tracking weather patterns, crop forecasts and trade flows. But one of the most important drivers of sugar pricing often sits outside agriculture entirely: the oil market.

At a time of geopolitical instability, particularly across key energy routes such as the Persian Gulf and the Red Sea, volatility in oil markets is feeding directly into sugar pricing, availability and supply chain risk. For buyers across the UK and Europe, understanding this relationship is no longer optional. It is essential for managing cost, continuity of supply and long-term procurement strategy.

In this article, we explain how oil prices influence sugar markets, how that relationship plays out across ethanol production, agriculture and global logistics, and what it means for food and beverage manufacturers.

Why global energy markets are now shaping sugar pricing and supply chains

The global sugar market is deeply interconnected with broader commodity and energy systems. Sugar is not just a food ingredient; it is also a feedstock for energy production, and it moves through complex global supply chains that depend heavily on fuel and transport infrastructure.

Recent geopolitical tensions have highlighted how quickly energy markets can shift. Disruption to oil supply, whether through conflict, sanctions or shipping constraints, drives rapid increases in oil prices. This has two immediate consequences.

First, it increases the cost of energy and transport across the entire supply chain. Second, it changes the economics of alternative fuels, particularly ethanol.

At the same time, supply chains themselves become less efficient. Shipping routes may be diverted, vessels repositioned and freight costs increased. While closing the Strait of Hormuz for example may not directly affect sugar shipments into Europe, disruptions in the Red Sea and Suez Canal can significantly alter shipping patterns, increasing transit times and costs.

For sugar buyers, this means price volatility and supply risk are not driven solely by crop fundamentals. They are also shaped by global energy dynamics.

The fundamental link between sugar and oil: ethanol economics

The strongest structural link between oil and sugar sits in ethanol production. In major sugar-producing countries such as Brazil and India, sugarcane can be used to produce either sugar for food markets or ethanol for fuel. The decision on how much cane is allocated to each depends heavily on relative economics.

When oil prices rise, ethanol becomes more competitive as a fuel. Governments may increase blending mandates, which means they tell industry, or through tax and legislative levers, how much sugar to use for ethanol production. Producers are then incentivised to divert more sugarcane into ethanol production. This has a direct impact on sugar supply.

When more cane is used for ethanol:

- Less sugar is available for export.

- Global supply tightens.

- Prices tend to rise.

When oil prices fall:

- Ethanol becomes less attractive.

- More cane is directed towards sugar production.

- Supply increases, putting downward pressure on prices.

Brazil is the clearest example of this dynamic. As the world’s largest sugar exporter, its production decisions have a significant influence on global prices. In high oil price environments, Brazil often shifts towards ethanol, tightening global sugar supply.

India shows similar behaviour, with government policy actively supporting ethanol blending. In recent years, this has led to reduced export availability during periods of high energy prices.

While the relationship is not perfectly linear and there is a lag between oil price movements and sugar price movements, the directional link and correlation is clear. Oil price movements create a floor or ceiling for sugar prices through ethanol economics.

Secondary impacts: how energy prices affect agriculture

Beyond ethanol, oil prices also influence sugar markets through agricultural inputs. Sugar production, both cane and beet, is energy intensive. Fuel and fertiliser are among the largest cost components in farming and processing.

When oil prices increase:

- Diesel costs rise, increasing the cost of planting, harvesting and transport.

- Fertiliser prices increase, as many fertilisers are derived from natural gas.

- Irrigation and processing costs increase due to higher energy prices.

This creates a complex response from producers. In some cases, higher sugar prices may encourage farmers to plant more. However, if input costs rise faster than output prices, margins can be squeezed, discouraging production. The outcome depends on regional conditions.

For sugarcane producers:

- Higher energy costs increase operating expenses.

- Ethanol demand may offset this by increasing revenue potential.

For sugar beet producers in Europe:

- Energy costs are particularly significant in processing.

- Fertiliser and fuel costs directly impact planting decisions.

These dynamics can lead to:

- Reduced planting in high-cost environments.

- Lower yields if inputs are reduced.

- Increased price volatility as supply adjusts.

In effect, energy markets influence not just how much sugar is produced, but how efficiently it is produced.

Shipping, logistics and the hidden impact of oil volatility

The third major link between oil and sugar markets sits in logistics. Sugar is a globally traded commodity, with significant volumes transported by sea from production regions such as Brazil, Colombia, Thailand, Mauritius, India and Australia into Europe and the UK.

When oil prices rise, shipping costs increase. But more importantly, geopolitical disruptions can fundamentally alter supply chains.

Recent events have demonstrated several key risks:

- Shipping routes can become restricted or unsafe, forcing vessels to take longer alternative routes.

- Ships may be in the wrong place at the wrong time, creating regional imbalances in freight availability.

- Port congestion can increase as trade flows adjust.

Disruptions in the Red Sea, for example, have led to rerouting around the Cape of Good Hope on the southern tip of Africa, adding significant time and cost to shipments.

These factors compound price pressures:

- Higher freight costs increase landed sugar prices.

- Longer transit times increase working capital requirements.

- Greater uncertainty increases risk premiums across the supply chain.

Within Europe, higher fuel prices also impact land and rail transport, further increasing distribution costs.

For buyers, these effects are often less visible than commodity price movements, but they can be just as significant.

What this means for sugar buyers

The key takeaway for sugar buyers is that sugar markets cannot be viewed in isolation.

Oil price volatility feeds into sugar markets through three interconnected mechanisms:

- Ethanol production and cane allocation.

- Agricultural input costs.

- Global logistics and transport.

This creates a more complex and less predictable pricing environment. At the same time, the way buyers interact with the market is changing. Price signals may move quickly, supply availability can shift regionally, and lead times may extend without warning.

However, these challenges also highlight a critical point. The ability to manage this complexity is what differentiates suppliers.

Price and specification will be key criteria for choosing a sugar supplier today. But so will:

- Understanding global market linkages.

- Managing sourcing across multiple regions.

- Navigating supply chain disruption.

- Providing continuity of supply in volatile conditions.

At Ragus, we monitor these interconnected markets closely, from energy and agriculture through to logistics and trade flows. This enables us to anticipate changes, manage risk and support our customers with reliable supply and informed market insight.

In a world where oil markets can influence sugar availability as much as weather or crop yields, that capability is essential.

Ragus supplies functional sugar ingredients to the food and beverage industry, with a deep understanding of global sugar markets, pricing dynamics and supply chain risk. We work closely with our customers to ensure continuity of supply, even in volatile market conditions. To discuss your sugar requirements or market outlook, contact our Customer Services Team. For more insight and market analysis, explore Sugar Talk and follow Ragus on LinkedIn.

Ben Eastick

A board member and co-leader of the business, Ben is responsible for our marketing strategy and its execution by the agency team he leads and is the guardian of our corporate brand vision. He also manages key customers and distributors.

In 2005, he took on the role of globally sourcing our ‘speciality sugars’. With his background in laboratory product testing and following three decades of supplier visits, his expertise means we get high quality, consistent and reliable raw materials from ethical sources.